Things are getting hairy in the economy

I feel kind of foolish writing a bearish commentary on the economy, but I feel like the economic conditions right now are screaming at us, and I don't see how our central planners are going to get us out of this mess. They are calling for "soft landings" or an outright cancellation of a recession. After all, we just went through a pandemic that destroyed production worldwide and we appear to have recovered to a position of stability.

I would argue however, that the pandemic opened a bunch of wounds still left open from 2008 and set into motion a financial crisis that could be much more severe than ons we have seen in the past. This isnt just any financial crisis brewing, this could be a world defining moment we are living through. What happens to our economy these next 5 years can really shape the future of the United States.

I am hoping we figure it out, but as they say, prepare for the worst and then anything that happens is a pleasant surprise. In this article i'll explain some of my biggest worries, my strategy going into this, and informational resources to help you do some research about the current environment we are in.

Whats led up to this point

I am sure you are well aware of the 2008 financial crisis. Just to share some basic economics, since then, the world's central banks have been influencing the markets using the "modern monetary theory". This allows central planners to set interest rates which affect how much people pay for debt in the capital markets.

:max_bytes(150000):strip_icc()/PrintingMoney-58b83d575f9b5880809b9a14.jpg)

For the last decade the federal reserve set near zero interest rates, causing capital to be artificially cheap. Due to this, it caused economic productivity and asset prices to sky rocket. Even before the pandemic and recent bull run, many were already calling this one of the biggest asset price bubbles in history. Real wages also grew drastically, making life very comfortable for all involved.

Then came the pandemic, where governments implemened a variety of economic policies and welfare services that are having lasting affects on the economy. One of the biggest of these policies was injecting the economy with massive amounts of cash, causing an asset bubble. This also caused inflation to no surprise, which triggered the federal reserve to follow its mandate to start jacking up interest rates and do quantitative easing.

This isnt anything too unusual or unexpected, the central banks intervention in the free market is common. This time however, interest rates were so low and inflation rising so fast they had to raise rates aggressively. This is like hitting a stop button on the economy and is causing a lot of issues mentioned further down in the article.

An interesting speculation

In addition to the money supply expansions, the governments also simultaneously shut down millions of businesses due to covid measures. These types of measures are not part of the standard monetary theory and caused our economy to behave unnaturally.

One of these situations that arose, is that the government allowed larger corporations to remain open during the pandemic, while small businesses shuttered. I believe this just funneled trillions into these corporations or assets, as citizens had little choice in how to pay for goods and services to these remaining larger businesses.

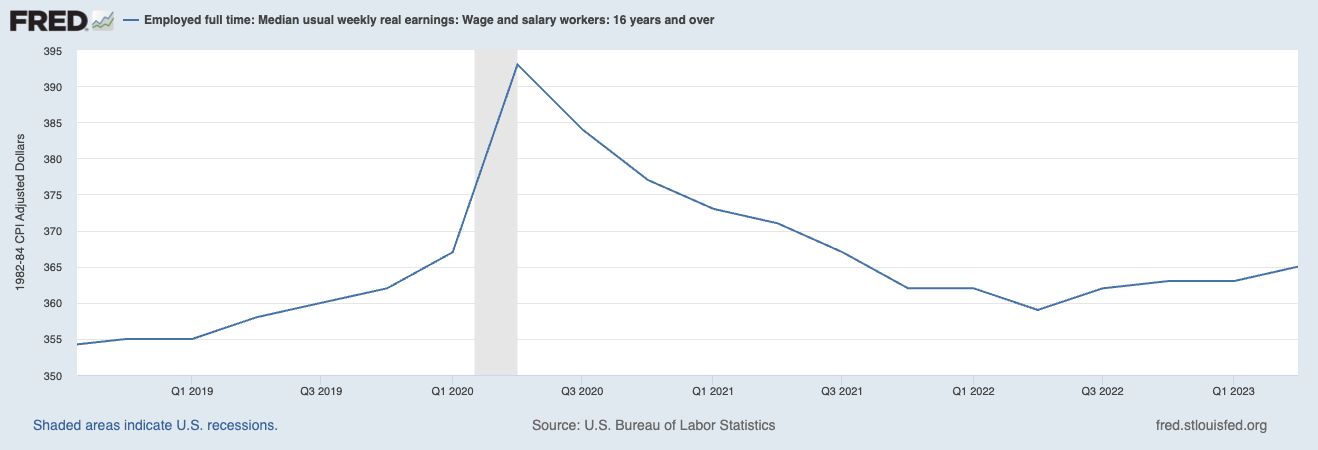

I believe this unique situation is causing side effects in our economy that we have not seen before. It certainly has not helped the real wages of Americans, which is a leading economic metric to watch.

If you believe wealth unequality is an issue, this also plays directly into Thomas Picketty's theory that capital returns will outpace returns on labor, which can lead to some dire consequences in the long run.

There are many other factors that led up to the point we are at yet, but I do believe this blundered wealth print and distribution hurt the middle class at the worse time and helped accelerate an implosion of the middle class in the economy.

The economy of paradoxes

If you learned macroeconomics in college, many of the models we were taught appear to be at odds with each other right now. The equilibriums charts are all out of wack from these interventions from the central planners.

On the surface, things dont look too bad. Unemployment is low, asset prices are still rising, inflation is dropping, and house values are some how holding on.

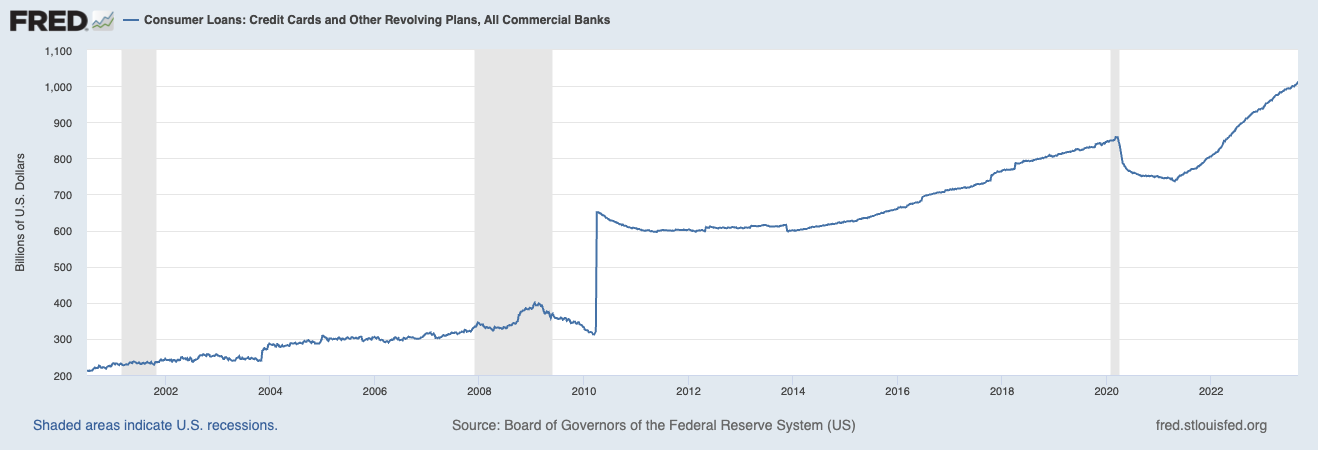

If you dive into other important metrics however, they paint a more dire situation. Debt for people and corporations is sky rocketing, demand is collapsing around the world, and inflation has been outpacing wage growth for years now. Americans spending power has effectively been in a decline now for 3 years already. Americans have been fighting inflation with sky rocketing debt levels, debt that they cannot afford at these high interest rates.

If we actually enter a recession where unemployment starts rising and capital continues to be restricted, I imagine this will turn out bad for an average person. Everyone might have their heads above the water now, but they are already kicking hard to stay there.

Macro Economic Headwinds

There isnt just one thing that causes an economic crisis. It is typically a series of minor events and situations that perpetually make everything worse. Feedback loops work both ways, and we are entering a negative feedback loop in the economic cycle. Completely uncorrelated crises are developing at the same time, and are causing a rippling effect through the economy as they indirectly cause other crises.

China Collapse

The most time sensitive story developing is in China, it is not looking short term there. Demand is falling from trading partners, and its causing exports and imports to crater. There is also mass unemployment of factory workers rising which shows how demand for their labor is falling.

Longer term, China also faces many issues such as their aging demographic issues, and more importantly their real estate market is failing. It cannot be overstated how important this real estate market is in China, its growth has accounted for much of the nations store of wealth. It's rise helped secure the power for many of the party members of the CCP as they were able to show economic growth despite other shortcomings. With this pillar collapsing, its hard to see a situation where the CCP holds onto China.

The world is far too globalized now to not be affected by such a major trading partner.

.jpg?itok=5x9qLhIM)

US Debt Crisis

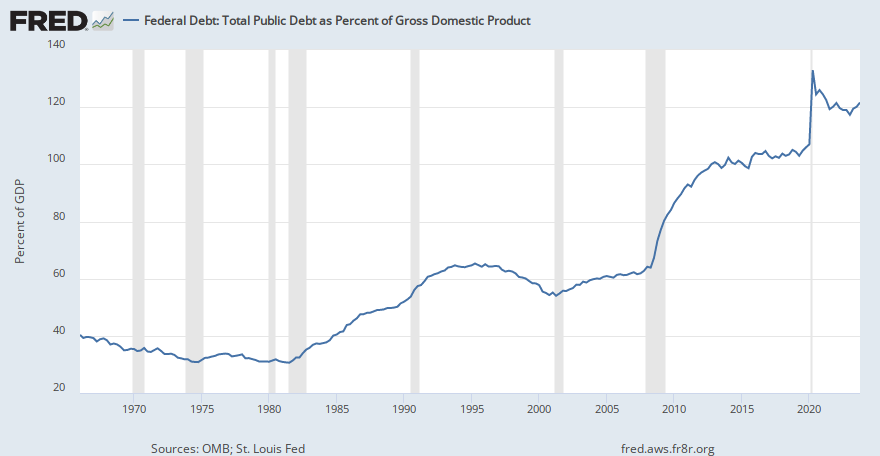

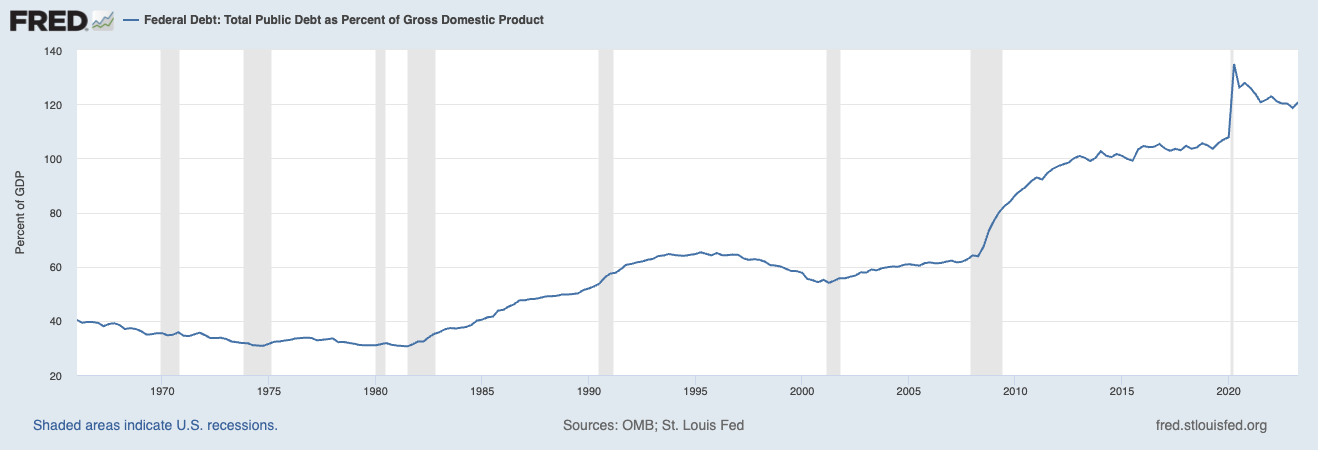

The US is now above the 120% debt to gdp ratio that is generally known as the point of no return for debt repayment. As mentioned, Americans are fighting inflation with debt we cannot afford.

At this stage its near impossible to not have an out of control interest situation in which debt payments outpace the amount of money available. Historically governments will try to print their way out of this, causing more inflation and destroying wealth.

In the next 10 years social security and other services are expected to run out of money. The US needs some serious economic productivity gains or austerity measures. Politicians are unable to even comment on this topic without being ridiculed so I dont see this getting resolve until its too late in about a decade. At that time we will be well past the point of no return.

Student Loans

Currently there are over 20 million Americans not paying student loans and the US is ending its student loan forgiveness program. This is going to massively start draining liquidity from the system starting October 1st. The capital markets are already strapped for cash so this will only put more downward pressure on the economy.

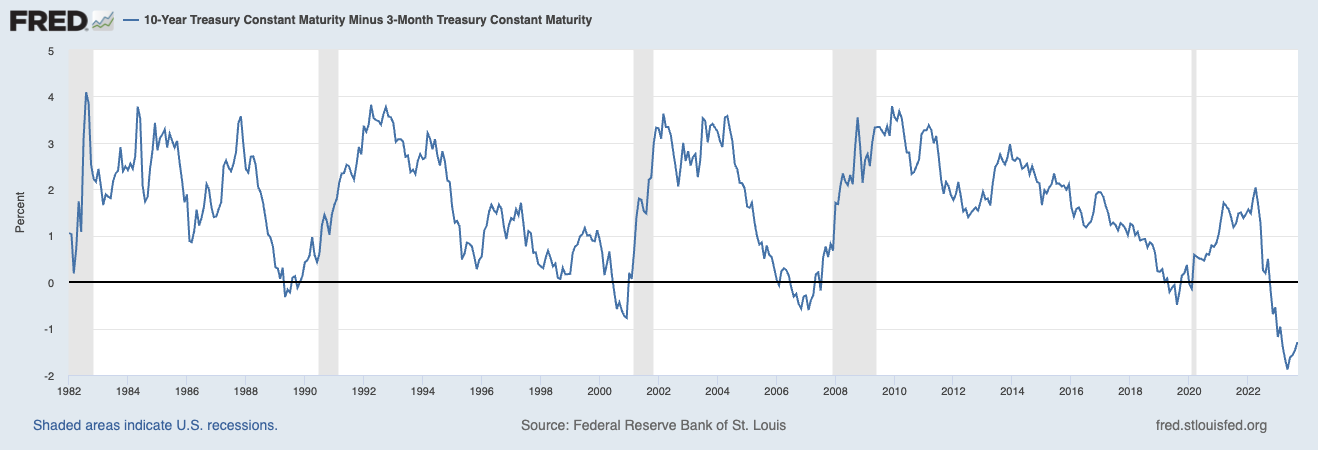

Credit Banking Crisis

Short story, banks have large unrealized losses on their balance sheets due to the value of bonds crashing with interest rates rising. Its not just a few banks failing, the entire system nationally and globally is under immense pressure right now from the central planners jacking up interest rates this quickly. This is also causing a credit crunch around the world as capital is drying up.

One quick way to gauge how the markets are doing is compare the longer term bond rates versus shorter time frames. When yields are higher on the shorter term bonds than the longer term, this generally marks the beginning of a recession.

There is also the subject of the global derivatives market which accounts for a large portion of the wealth generated in the economy as banks swap risk with each other across nations. With dollars becoming more scarce, there is going to be a massive margin call that will leave many financial institutions in dire situations as they need to come up with these assets.

Real Estate Market

Real estate is obviously in a world of hurt right now with interest rates so high, especially the commercial sector. The pandemic and remote work movement put downward pressure on office space and properties that are dependent on this type of market. With values plummeting, commercial owners are underwater on their loans and will need to finance new terms with banks at the higher interest rates.

Higher prime interest rates affect commercial investors as these funds are on variable interest rate loans, or on shorter loan terms with banks. This means that they may need to constantly lend for projects every 5 years. At this time, this means a massive increase on the base interest they were lending at before, causing the rate of capital return to lower on these investment properties.

These types of investments are dependent on debt and have precise debt to equity calculations to see which deals are worth it. If the ROI, or capital rate of return is too low due to debt interest being higher, I suspect a lot of these companies are just going to let these properties foreclose, causing the banks to be left holding the bag.

Regarding private real estate, markets have also been having downard pressure on prices as mortgage rates are now unaffordable for most Americans. There is also the issue of Airbnb's not returning the same amount of dividends they did before, causing all those properties to fire sale as optimistic property owners go under. When a few properties selling at discount can set prices for thousands of homes, this is going to cause many houses to loose significant value.

Despite these short coming, I dont think private real estate market is at much of a risk for a sharp correction. My best guess is that markets will slowly decline over the next few years. People are going to be holding on for dear life to their low interest mortgages until markets normalize again. This should cause supply to continue to be strained, which can help stabilize prices even in a downturn.

Megan Henney

Megan Henney

BRICS

There is a growing anti dollar sentiment growing around the world from countries that are sick and tired of the US interfering with their economies and its competitive advantage it has as the worlds reserve currency.

I actually dont think this is a big deal, the rest of the world is a shit show right now, if a massive world order shift is in play, they definitely are not going to happen anytime soon. I think India is showing the most promise, but it has a long way to go before it starts competing the top superpower economies. The country is still very much a developing country.

A threat to the US economy however shouldn't be ignored. I personally already have a lot of international exposure due to the nature of my business, so I dont feel the need to diversify from US assets but I could see the concern people have.

Carien du Plessis

Carien du Plessis/cloudfront-us-east-2.images.arcpublishing.com/reuters/EHWMEOHYHZOV7MRL6SABRMFDKM.jpg)

Ukrainian War

Its kind of strange that this war is not in people's minds anymore. Its still very much a major conflict that can risk world war, but also is putting downward pressure on European economies as they face uncertainty and war time economic sanctions.

This can be shown by how its affecting Germany, one of the powerhouses of the world. Germany is having a tough time.

So whats the plan?

One thing I read early on in my life that stuck with me about investing is always have a testable hypothesis and a plan for an investment. This way you always have a solid plan for what you are doing, and more importantly a framework to study if you are wrong so that you can continue to learn.

My best guess is we will have a down turn within 3-6 months, then the fed will be forced to start lowering rates again within a year. Here are some good videos you can start with to learn more about our economic situation.

Growth Investments

Im not so bearish that ill stop dollar cost averaging into my existing investments.

- $100 weekly into Crypto BTC - Im still very bullish on crypto

- $125 into my M1 Portfolio - Dollar cost average long term fund

- $100 into Dividend Stocks weekly - Instead of into AI stocks. I stopped buying AI stocks for the meantime as they seem aggressively overbought right now. Belo is my reasoning on this.

Dividend Stocks

With T-Bills and other similar investment vehicles paying 5-6%, people and institutions are just plowing money into government funds. Its practically a risk free investment, which makes it great for many types of investors that end goal is just to lose other peoples money.

This draw of liquidity into bonds negatively affects dividend stocks prices, as they are competing products in the category of dividend income. Why would you risk losing money due to depreciation at a 4% return, when you can park your money with the government and get 5% risk free?

Another effect from this on dividend stock prices, is that they are also highly susceptible to difference in interest rates, in that dividend producing companies are very reliant on debt for operations. When we are in these high interest environment, prices are being supressed due to the competition with bonds, and also operations are more expensive.

This makes it a perfect storm and I feel that dividend stocks are highly undervalued right now due to these excessive downward pressure. These stocks are trading at almost all time lows with low PE ratios.

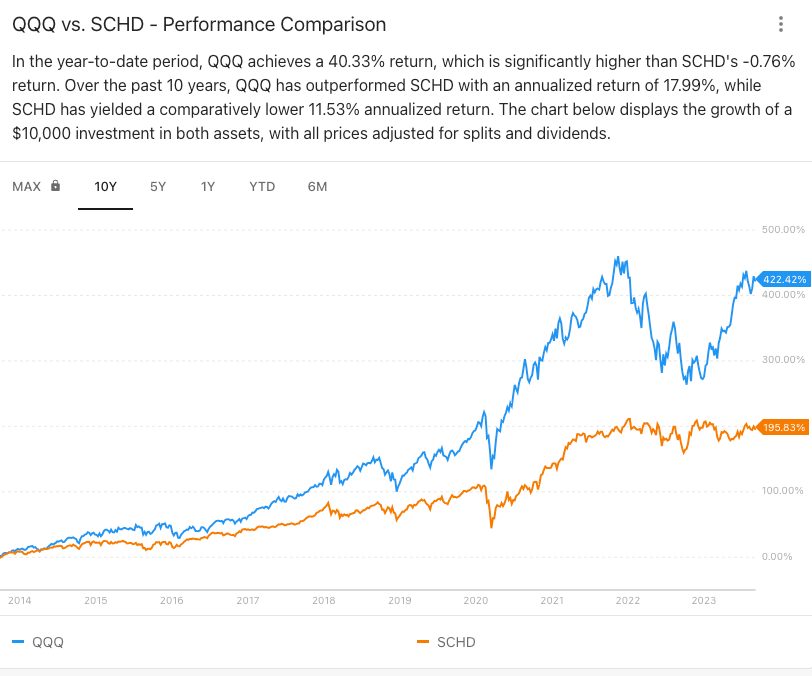

Look at the spread between QQQ and SCHD, to me this shows there is a good chance at high dividends + appreciate this next 1-2 years.

Top Stock Picks

Here are companies that I picked that have a solid track record, I understand them, they have a high dividend yield, and most importantly they are extremely undervalued right now. For reference with a 2.5% inflation rate, a PE of 25 is considered normal, the market has really battered down these stock prices.

- Walgreens - 5.49 PE - Yield 8.73%

- At&t - 5.98 PE - Yield 7.7%

- Verizon - 7.09 PE - Yield 7.9%

- CVS - 7.6 PE - Yield 3.68%

- Pfizer - 10.38 PE - Yield 4.79%

- Target - 16.28 PE - Yield 3.56%

- SPG - 18.89 PE - Yield 6.63%

I should note, my main M1 portfolio also has a 30% allocation to SCHD and JEPI. Which are dividend focused funds in addition to these individual picks. These are in the portfolio to provide dividends into the other growth slices as the portfolio rebalances.

- SCHD - 3.49% Yield. My favorite dividend appreciation fund.

- JEPI - 10% yield. This is probably too greedy, dont do this.

Cash is King

In a bearish case, the obvious choices here is to save cash, pay off your debt, and try to maintain your income streams. As a regular ass dude however, I know im going to mess this up and become another panicked citizen. My income stream is my own small business, meaning an economic downturn is not going to be a pleasant experience for me. I am really going to try to take this more seriously this downturn. Fortunes are made in recessions if you can remain disciplined.

The first thing I am doing is actively try to reduce my expenses. I am planning on hunkering down in Mexico the next 4 months and just earn / save as much money as possible. I canceled most of my business trips and other frivolous things. The cost of expenses are cheap in Mexico, my rent is only $400 a month, and if a crisis hits, the dollar should rally against the peso making expenses dirt cheap.

I have an auto transfer once a week for $425 into my M1 Savings account, which has around a 5% interest rate right now. This should handle all my monthly payments and expenses.

T Bills

Next up are the magic t-bills all the cool kids on the block are talking about. These are going to be my secret to making sure I have cash flow when my income stream is negatively affected by these downturns. Buying treasury bills to force me to save cash for the future.

I am terrible at saving just cash, and reminds me of a warren buffet saying:

The lesson for investors, Buffett says, is that you don’t have to swing at every pitch.

The trick in investing is just to sit there and watch pitch after pitch go by and wait for the one right in your sweet spot. And if people are yelling, ‘Swing, you bum!,’ ignore them.

When markets are crashing, its hard to be disciplined. I would rather just secure that cash now, and unlock it if my prediction comes true in the next 3-12 months. There is an argument to be made that I should just invest this all now, but I am a big advocate of dollar cost averaging. Its the only way I can guarantee I hit the bottom and give me more time to focus on keeping my business humming.

I am laddering 4 different T-Bill with varying maturity timelines that I will keep auto reinvesting until markets start showing stress. This is effectively setting up an investment stream ahead of time based on a predetermined strategy. This could epically fail and lock up my cash at prime opportunities, but interest rates are almost 6% so it could be worse.

T Bill Strategy

4 week t-bills - $1200 total - Rent Payments - I am going to pay double rent for the next three months, by buying an equal value t-bill to my rent. I will then keep them rolling over each month until I am in a position where I need to either pay rent or keep investing.

13 week t-bills - $4000 total - $350 a week for 3 months - If markets do take a turn in the next few months, this is going to be the dry powder ready to go. Otherwise ill keep it reinvesting on 13 week intervals.

26 a week t-bills - $200 a week - 26 weeks is when I expect the markets to start hitting better buying opportunity. Business will be hurting and I want these payments to keep the purchasing going in the markets.

52 Week t-bills - $500 a month - Once I finish buying my 4 week and 13 week, I will do these purchase once a month. If things get bad, I want this on the sideline to keep for expenses. With this much of my spending power going into the markets like this, and if we are actually in a bad economy, my business is probably going to suffer. I might need this to squeeze out the recession.

Time Frames Organized a bit better

- Week 0 - Markets start taking a turn down, ill continue buying assets using my normally DCA strategy but turn off the reinvestment of t-bills.

- Week 4 & 8 - Unlock a monthly expense payment to help cover rent

- Week 13 - 26 - Unlock larger payments for 3 months to invest with. If we are in a down turn, this should be a great buying opportunity.

- Week 26+ - Unlock smaller continuous payments to continue DCA for indefinite future.

- Week 52+ - Unlocks larger monthly expense payments

Using this strategy, the ideal time for the market to crash would be Feb of 2024. I have a feeling its going to crash much sooner though, with credit tightening so fast, its hard to see the markets not panic before then.

What if im wrong? Not a big deal, saving up cash is much better than spending the cash! If you somehow made it this long in my ramblings, here is one last video that explains the case if a market crash doesnt happen.